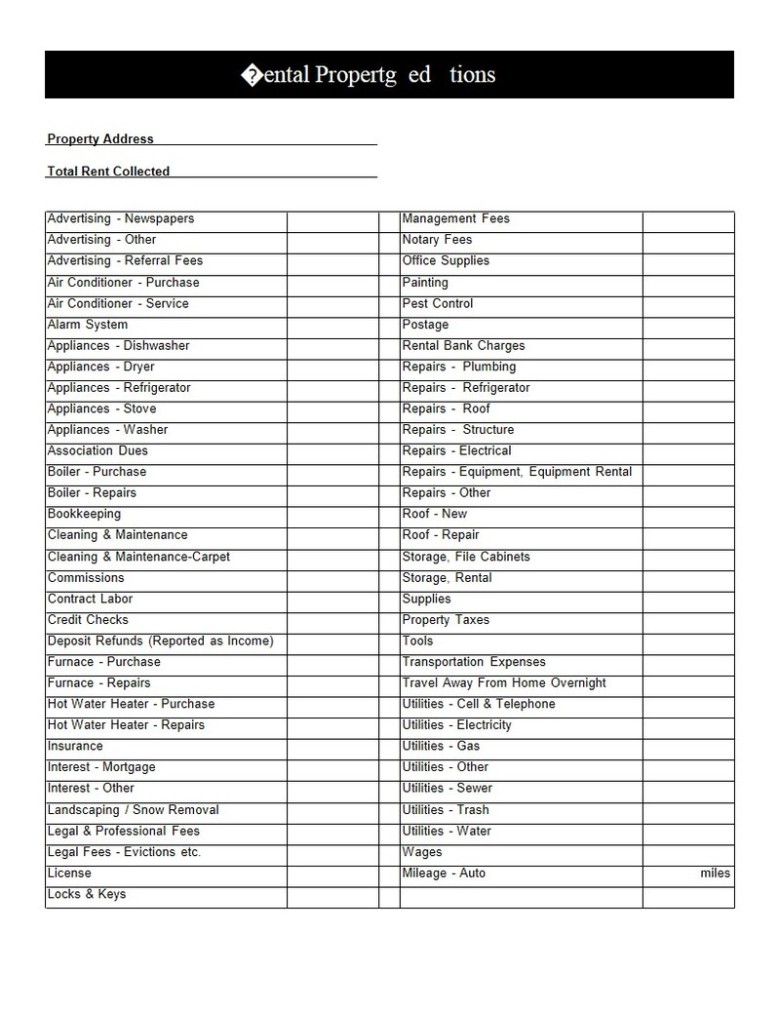

Table of Content

So, if you claim a 200 square foot office, that multiplied by the IRS rate is $1000. There's a lot of talk about an audit risk for the home office deduction. This is because many small business owners tried to take advantage of this tax write-off when it was first introduced. You'll just need to measure the square footage of your home office in which you use as your principal place of business and exclusively for business. Your home office space has to be used solely for conducting business activities. Even after you file your taxes, save all tax-related records for as long as the IRS might want to look at them.

With this option, you can claim home-related expenses such as rent, mortgage interest, utilities, insurance, repairs, and other expenses. This option allows for a standard deduction of five dollars per square foot up to a maximum of 300 square feet (for a maximum deduction of $1,500). This method allows the full home-related itemized deductions on Schedule A, such as mortgage interest and real estate taxes .

Resources for Your Growing Business

A business owner can calculate home office deduction using two methods— regular and simplified option. Under the regular method, you'd use Form 8829 to determine your deduction using figures for the area of your home and total hours it was used for business purposes, your business income and other business expenses. When using the regular method, deductions for a home office are based on the percentage of the home devoted to business use. Taxpayers who use a whole room or part of a room for conducting their business need to figure out the percentage of the home used for business activities to deduct indirect expenses.

Administrative or management activities i.e. billing customers or clients, ordering supplies, setting up appointments. You may have to do a few more calculations to get the total deduction amount. See the worksheet on page 25 of IRS Publication 587 for the rest of the calculation. The home office deduction, calculated on Form 8829, is available to both homeowners and renters. Segregate personal activities from the home office area. Move all home office furniture and equipment to one specific area.

Insurance

However, once you have elected a method for a taxable year, you cannot later change to the other method for that same year. Any expenses for maintenance or repair or other aspects of your home, such as landscaping, that do not pertain directly to your home office, are not eligible for home office deduction. The Tax Cuts and Jobs Act eliminated home office deductions for any W-2 employees starting 2018, through 2025. You must be in the business of providing care for children, for elderly individuals age 65 or older, or for individuals who can't care for themselves due to physical or mental impairments.

No depreciation deduction allocated to the space used for the home office or later recapture of depreciation is allowed. To meet the exclusive use test, a taxpayer must have a specific part of the home—though not necessarily a complete room—set aside and used regularly and exclusively for business purposes. The area is not limited to a single room; multiple rooms may qualify.

Highlights of the simplified option:

The basis and the amount realized must be allocated between the home and the business portion of the property and the sale of the business portion must be reported on form 4797. For more information see IRS Publication 523, Selling Your Home. To qualify under the trade or business test, the area of the home must be used in connection with a trade or business, not merely a profit-seeking activity. For example, if a taxpayer is not a broker or dealer but merely making investments of his own, then a deduction is not allowed for the area used.

The home office deduction limit depends on your gross income—Form 8829 will help you figure out your limit. If your home office meets these qualifications, then you may be able to write off the following items on your taxes. Deducting these expenses will help reduce your total taxable income and save you money. An ITIN is an identification number issued by the U.S. government for tax reporting only. Having an ITIN does not change your immigration status. You are required to meet government requirements to receive your ITIN.

Can You Deduct Business Use of Your Home Expenses?

Lawmakers worried that the Scott case could allow home-office deductions that could cause an increase in a business-loss deduction. Both options involve figuring your expense onForm 4562, Depreciation and Amortization. It's referred to as aSection 179 deduction and is calculated in Part 1 of Form 4562 if you want to take the full deduction in the year of purchase. You're "depreciating" your property if you decide to spread out the cost over a number of years.

The amount you can deduct related to casualty losses are calculated based on the adjusted value of your home or its decrease in value. Or the total amount of loss, if the home is destroyed. In fact, a few states require employers to reimburse their employees’ necessary out-of-pocket expenses as a result of their job duties. Those states include California, Illinois, Iowa, Massachusetts, Montana, New Hampshire, New York, Pennsylvania, South Dakota and the District of Columbia. Federal pricing will vary based upon individual taxpayer circumstances and is finalized at the time of filing. You conduct administrative or management activities at places that aren’t fixed locations of the business, like in a car or a hotel room.

Not all indirect expenses may be included in the allocation. For instance, utilities and services not used in the business, lawn care, and the first telephone line to the house all must be excluded. An example of an excluded utility would be propane gas supplied for cooking on the kitchen range. Any expenses that are only used for the home office are entirely deductible.

Only self-employed workers and independent contractors can still claim a home office deduction as a Schedule C business expense. Enrollment in, or completion of, the H&R Block Income Tax Course or Tax Knowledge Assessment is neither an offer nor a guarantee of employment. There is no tuition fee for the H&R Block Income Tax Course; however, you may be required to purchase course materials, which may be non-refundable.

No comments:

Post a Comment